How to Sell them

The strategies, scripts, and approach to confidently present ancillary products to your clients.

How to Sell Hospital Indemnity (HI)

The Gaps Medicare Advantage Leaves Behind

MA plans cover major medical, but clients still face uncovered costs. Here's what they're exposed to:

🏥 Hospital Costs

- ✗ Daily copay: $345–$375

- ✗ 4-day stay = $1,400–$1,500

- ✗ ER visit copay

- ✗ Ambulance copay

- → Solution: HI pays daily benefit

🎗️ Non-Medical Crisis Costs

- ✗ Lost income ($5K–$15K)

- ✗ Travel for care ($2K–$5K)

- ✗ Home help/childcare ($3K–$10K)

- ✗ Equipment, wigs, etc. ($1K–$3K)

- → Solution: Cancer CI lump sum

🏠 Recovery Care Gap

- ✗ SNF Days 1–20: $0 (MA covers)

- ✗ SNF Days 21+: $218/day client pays

- ✗ Home care: $150–$300/day

- ✗ Average recovery: 30–90 days

- → Solution: STC bridges the gap

Why HI Matters Right Now

The Bottom Line: MA-only revenue resets every October. HI and other ancillaries add a second income stream that renews independently—and outlasts plan changes.

The Three Essential Products

🏥 Hospital Indemnity (HI)

The Gap: Daily hospital copays of $345–$375 add up fast. A 4-day stay = $1,400–$1,500 out-of-pocket.

What It Pays: Cash daily benefit ($150–$350/day), ER, ambulance, observation—pays client directly.

Commission: $96–$220 per policy

Premium: $45–$90/month

→ Lead product

🎗️ Cancer / Critical Illness

The Gap: 1 in 2 men, 1 in 3 women face cancer. Average cost: $150K medical + $11K–$33K hidden costs.

What It Pays: Lump sum ($5K–$7K) on diagnosis. Client decides how to use it.

Commission: $65–$175 per policy

Premium: $25–$60/month

→ Combo with HI

🏠 Short-Term Care (STC)

The Gap: 70% of seniors need care. MA covers SNF to Day 20, then stops. Average recovery: 30–90 days.

What It Pays: Daily/weekly benefits for home care, assisted living, skilled nursing (Days 21+).

Commission: $300–$720 per policy

Premium: $75–$150/month

→ Highest income

Discovery Questions (Six Key Asks)

Education-first approach closes 2x the rate of product pitches. These questions open the conversation:

"What happens in your house when a $1,600 bill arrives?"

Opens without selling

"How would a 5-day hospital stay impact your budget?"

Real-world impact

"Which bills come first—rent, utilities, groceries?"

Forced choices reveal gaps

"How comfortable are you with a large bill arriving at once?"

Comfort level → right tier

"Lower copays or flexible cash you control?"

Most pick flexibility (HI wins)

"What dollar amount feels stressful—$300? $1K+?"

Stress threshold

Then ask: "Based on what you've shared, I have a simple option that might fit. Would it be okay if I walked you through how it works?"

Never pitch before they're heard.

Walk the Gaps Line by Line

During your appointment, go through each gap with your client. Ask: "Does this match what you understand about your plan?" Then say: "I have a Hospital Indemnity plan that covers exactly this."

| SERVICE | YOUR MA PLAN PAYS | YOU PAY * | HI BRIDGES THIS |

|---|---|---|---|

| Inpatient Hospital | Covered after copay | $345–$375/day, Days 1–8 | Daily hospital benefit |

| Emergency Room | Covered after copay | $115–$130/visit | ER rider / lump sum |

| Ambulance (ground or air) | Covered after copay | $115–$130/trip | Ambulance rider |

| Outpatient / Observation | Covered after copay | $272–$450/event | Observation rider |

| Outpatient Surgery | Covered after copay | $272–$450/procedure | Day-surgery rider |

| Skilled Nursing (Day 21+) | Different/day after Day 20 | $218/day | STC or extended HI |

| Max Out-of-Pocket (MOOP) | Stops at $4,250–$9,250 | Up to $9,250 possible | HI avoids reaching MOOP |

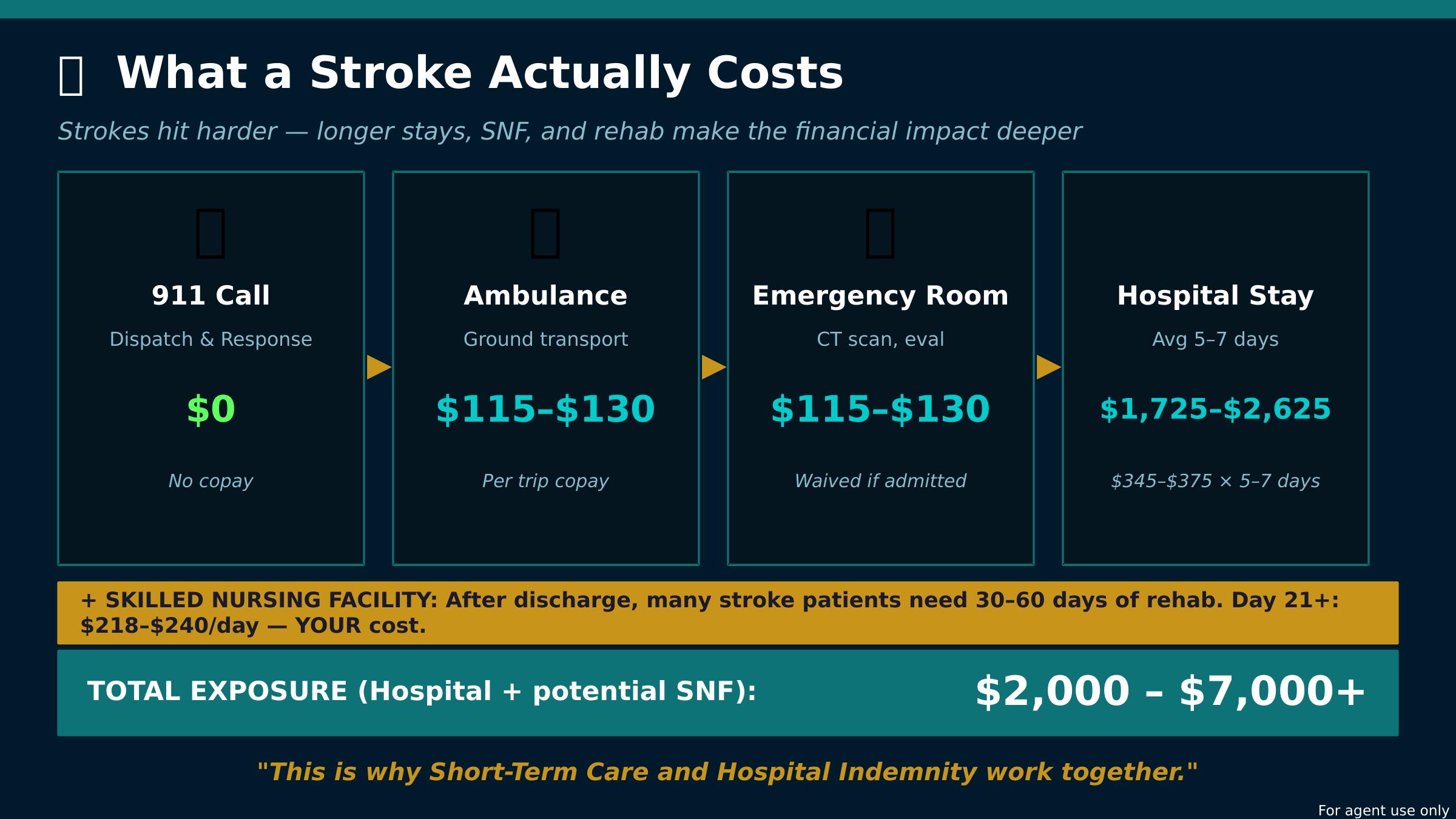

Real Cost Scenarios: Heart Attack & Stroke

Show your client these exact scenarios. Print or share before your appointment so they see the real dollar impact.

After showing: "This is a real scenario. The question isn't whether this will happen—it's whether they're prepared if it does. That's what Hospital Indemnity is for."

Run 3 Quotes

Prepare before the appointment

Your Three Quote Options

Option 1

$75–$80/month

Full Coverage

- ✓ $300–$350/day hospital

- ✓ ER + Ambulance

- ✓ Outpatient surgery

- ✓ Optional cancer rider

→ Lead with this

Option 2

$40/month

Mid-Range

- ✓ $150–$200/day hospital

- ✓ ER + Ambulance

- ✓ Core coverage

- ✗ Limited extras

→ Most popular

Option 3

$15–$20/month

Cancer or CI Only

- ✓ Cancer lump sum

- ✓ $5K–$7K on diagnosis

- ✓ First-day coverage

- ✓ Standalone option

→ Budget option

30-Day Action Plan

Week 1: Know Your Products

- Pick top HI carrier, learn quote tool

- Test quote: 70F, non-smoker (baseline)

- Get SOA templates ready

- Schedule carrier training

Week 1–2: Identify Prospects

- List 5 MA clients who'd benefit

- High MOOP? Recent health event?

- Concerned about medical bills?

- Stay CMS-compliant (product education)

Week 2–3: Practice Conversation

- Use 6 discovery questions on 2–3 clients

- Reflect back what you hear

- Don't interrupt—let them talk

- Walk through cost scenarios

Week 3–4: Close First Policies

- Conservative: 2 talks/week = 8–10/month

- Aim 25–30% close (2–3 policies)

- Aggressive: 3 talks/week = 12–15/month

- Document everything (SOA, needs)

Why This Matters

Protect clients from real MA gaps

Build a practice that doesn't reset Oct 15

Increase income without extra work

Stay compliant by design

Create referrals naturally

Win in 2026 by solving real problems

How to Sell STC

Content coming soon

How to Sell Other Products

Content coming soon